THE MUST-HAVE CONVERSATIONS WITH YOUR INSURANCE AGENT!

RENTAL PROPERTY INSURANCE –PROPETY COVERAGE |

|

| Proper Investment Valuation: | __________ |

| The Coverage Form – DP3- What’s Covered: | __________ |

| Loss Settlement Option for Home: | __________ |

| Deductible: | __________ |

| Water Backup of Sewer or Drains Coverage: | __________ |

| Earthquake: | __________ |

| Flood: | __________ |

| Building Code Upgrade Coverage (Ordinance and Law): | __________ |

OTHER STRUCTURES |

|

| Value of Other Structures (Garages, Fences, and other structures): | __________ |

LANDLORD FURNISHINGS |

|

| Value of landlord contents (Appliances, Furnishing) | __________ |

| Loss Settlement Option for Property | __________ |

LOSS OF USE/LOSS OF RENTAL INCOME COVERAGE |

__________ |

RENTAL PROPERTY INSURANCE-LIABILITY COVERAGE |

|

| Liability Insurance sufficient to cover your assets: | __________ |

| Premise Liability: | __________ |

| Personal Injury Coverage: | __________ |

| Medical Payments: | __________ |

| Umbrella: | __________ |

| Loss Assessment: | __________ |

ANNUAL PREMIUM |

__________ |

Why we use a Rental Property Insurance Checklist

Insurance can be mystifying. Many people have described it as a completely different language. Insurance is really just a complicated legal contract between you and the insurance company. The insurance company is bound to respond per the contractual terms, but because it is explained in legal terms it really is a different language, which is why many people fail to even put for the effort in understanding their insurance policy. While it is true that insurance policies are complicated, we at Gila Insurance believe there are some core things that every customer should understand, which is why we have created this checklist.

This checklist is designed to help you have the conversations with your insurance agent that will allow you to know what is covered BEFORE you have a claim. No checklist is fully comprehensive, these are things we believe are important that you understand, but please read your policy to ensure there are other questions that you have. The best time to understand your policy is BEFORE YOU HAVE A CLAIM.

If you are shopping for landlord insurance start your quote now, and let us quote several companies for you or check out some of our other landlord specific content.

Gila Insurance Group LLC specializes in insuring rental properties, Fix & Flips, Manufactured Homes, and Vacation Rentals, if this is what you do, give us a shot and get a quote today!

Insurance is complicated but understandable if broken down into small portions. That’s what we try to do. It’s rental home insurance coverage simplified, really!

RENTAL HOME INSURANCE COVERAGE SIMPLIFIED… REALLY

Let’s be real about the insurance purchasing process for investors. You know you need it or more likely your lender requires it, so you buy it. You work through the process with an agent that asks way too many questions, half of which you’re not sure of (you just bought the property, you don’t know when the roof was replaced, or plumbing and electrical was updated), you muddle through only to get a big stack of papers which you may or may not intend on reading, but is seemingly complicated and convoluted. Look, what I am about to write doesn’t apply to every policy. The best way to know what is insured is to read your policy. This doesn’t replace that, but hopefully, it can demystify things and make your insurance policy understandable.

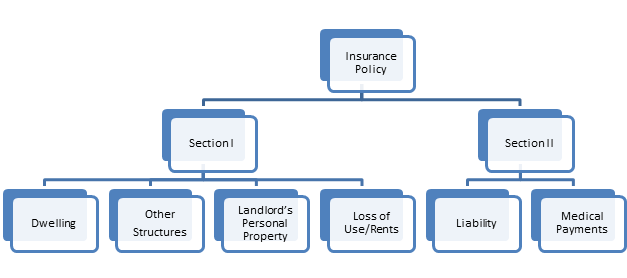

While there are MANY parts to a policy, there are only two sections. Hopefully, we can break it down into understandable bite-sized pieces, and not bore you to death in the process. I hope it’s not too late for some of you. I know some are visual learners, so let me break down a policy visually.

That’s it… kind of… two sections; 6 coverage parts, plus a bunch of extras. For example, there’s the declarations page, the insuring agreement, definitions, perils insured against, exclusions, and conditions… for both sections. Simple right? RIGHT! Baby steps. If you can understand this diagram, you are well on your way to understanding the coverage that you have.

To get an incredible quote these coverage sections start our online quote form. To talk to a licensed agent about this coverage call us at 1-877-784-6787.

This coverage explanation is for illustration purposes only and is general in nature. Coverage explained here may not apply to your policy, State, company, or situation. For more information about how your policy would respond in the event of a loss, please refer to the terms and conditions and declarations page of your policy.

Do you need to update your insurance policy?

Ahh summer time. A time of fun, sun, and DIY projects around the house. The extra light in the evenings lends itself to getting stuff done. So, I have a question: What did you do this summer? Maybe you’re not a DIY sort of person. Maybe you had a contractor or handyman do it for you.

Ahh summer time. A time of fun, sun, and DIY projects around the house. The extra light in the evenings lends itself to getting stuff done. So, I have a question: What did you do this summer? Maybe you’re not a DIY sort of person. Maybe you had a contractor or handyman do it for you.

Did you add a shed? Did you add on to your home? Did you add a block fence or a pool? Heck did you buy a new car? Did you get Married? Did you get a new Girl Friend?

Now for the most important question: Did you tell your insurance agent?

What Why would I do that, dude’s a square (and clearly uses insults from the 1950’s… loser).

Because it can affect your insurance. Consider this lesser known insurance clause:

Your house has to be insured to at least 80% of its value or you can be penalized in the event of a claim.

Yes penalized. Well that wouldn’t happen to me. Did you tell your insurance agent about your addition? Because if not, you just change the ratio of the insurance coverage to the value of your house.

“Well, I just added a pool.” Will your insurance company cover you if you have a pool? Some don’t or have strict rules about fences.

Did you get married? You probably need to make sure your spouse has been added to the policy? You also need to combine your policies for savings purposes. Finally, do you need to cover that rock you just bought her? There may be coverage on a homeowner’s or renter’s policy, but there may not be depending on the value.

If your girlfriend just moved in with you did you know that she may not be covered if she drive’s your car? Or that coverage can be limited? (this can vary GREATLY by company).

See. Your insurance agent may be a goober, but you need to tell him or her stuff because if you have done something to your cars, home, or if you have just had some changes in life, talk to us about how that impacts your insurance needs. He/She can help you anser the question do you need to update your insurance policy.