HOW TO FILE AN INSURANCE CLAIM

Insurance claims don’t have to be difficult. They are never going to be convenient, but they can go smoothly. Knowing what to expect is half the battle, and being proactive can help things move along. There are a few basic steps in the claims process.

- Preparing to call – Before you call to file your claim it doesn’t hurt to have a few things on hand to make the process go smoother.

- Your Policy Number

- The date the loss happened

- A description of what happened

- Your contact information

- Contact information for any witnesses or other people involved.

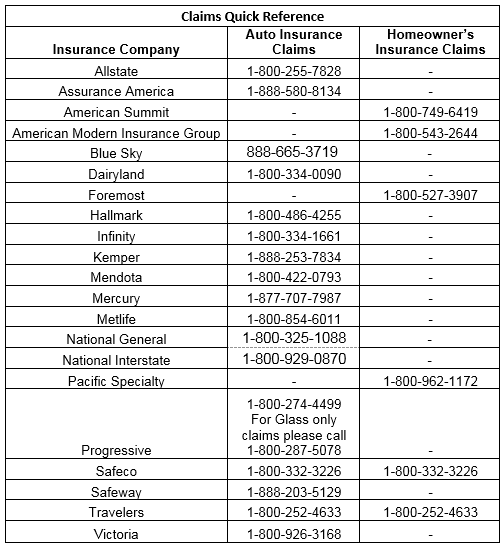

- Filing a claim – As soon as you have had a claim you will need to file it with your company. Today that can be done in a number of different ways. Sometimes the easiest is to simply pick up the phone. Below are phone numbers for each of the companies that we represent.

- Getting an Adjuster – Once you have filed your claim you will be assigned an adjuster that will handle your claim. Depending on the type of claim this could be a team or an individual. Once you have filed your assigned adjuster will reach out to you to introduce themselves and explain the process related to your claim.

- Gathering information – The adjuster’s responsibility is to gather information about the claim, determine the value of the loss, make sure that coverage applies to the loss, and to settle the claim. They will ask lots of questions, explain coverage, and suggest ways to minimize further damage. If needed they might schedule an appointment to come review the damage.

- Estimating the damage – Once it has been determined that your loss is covered they the adjuster will work with you to get estimates for repair.

- Settling the claim – Once estimates for repair have been received, the company will then pay you for the loss (remember there will be a deductible).

- Closing the claim – Once the claim has been paid, the claim will be closed. If there are additional costs related to that claim, your claim can be reopened to investigate if coverage applies.

HOW LONG WILL YOUR INSURANCE CLAIM TAKE TO CLOSE?

It depends on how complex of a claim it is, so ask the adjuster when you talk to them. Staying on top of things, getting estimates in a timely manner can have a big impact on how quickly it takes to close the claim.

Some coverage is hard to explain, it’s much easier to just say see! That is exactly the case with debris removal. Debris removal isn’t difficult to explain, it’s just the cost to remove the pile of trash your insurance claim just left. If there is a fire, it’s going to be the ashes and rubble, but also the mess the fire department caused while putting it out. Let’s be real they are great a putting out fires, but they aren’t exactly tidy. If there is a flood, we might be looking at all the damaged drywall and installation. Some of it might be moldy or muddy. The point is there is a cost to haul it away. But there is also going to be a cost for the demolition, which can get pretty costly.

Some coverage is hard to explain, it’s much easier to just say see! That is exactly the case with debris removal. Debris removal isn’t difficult to explain, it’s just the cost to remove the pile of trash your insurance claim just left. If there is a fire, it’s going to be the ashes and rubble, but also the mess the fire department caused while putting it out. Let’s be real they are great a putting out fires, but they aren’t exactly tidy. If there is a flood, we might be looking at all the damaged drywall and installation. Some of it might be moldy or muddy. The point is there is a cost to haul it away. But there is also going to be a cost for the demolition, which can get pretty costly.

Recently near my office there have been two fires. The first was in a second level apartment. The second was in a single-family home rented to a young couple. It was on one of my many strategy walks that I decided to explain debris removal through picture.

Debris removal is usually included in most property insurance policies, but like most things with an insurance policy there are limits. Depending on where it is commercial insurance or a homeowner’s policy it can vary, but here are some things to consider when it comes to debris removal. How unique is your building? How old is your building? How much space is around your building. All of these and more can cause additional costs in removing debris from your property. Another consideration is building materials. Is there any asbestos in the building? The cost of asbestos disposal adds additional cost to debris removal.

Debris removal is usually included in most property insurance policies, but like most things with an insurance policy there are limits. Depending on where it is commercial insurance or a homeowner’s policy it can vary, but here are some things to consider when it comes to debris removal. How unique is your building? How old is your building? How much space is around your building. All of these and more can cause additional costs in removing debris from your property. Another consideration is building materials. Is there any asbestos in the building? The cost of asbestos disposal adds additional cost to debris removal.

As is not unusual, insurance policies provide coverage for a number of different situations that you probably hadn’t even considered. While we may often complain about insurance the truth is that the benefits provided by our insurance policies are amazing.

Insurance companies can rightly be described as technological dinosaurs. I mean for years one company has been extolling the virtues of getting a quote in 15 minutes. On a side note did you know you can get a quote from multiple companies on GilaInsurance.com in just a few minutes as well? Again, dinosaurs. I mean my patience for 30 second in a microwave is almost nil. Don’t even get me started on when the internet decides to have a traffic jam (super highway. It’s supposed to be a super highway, that means no buffering, right?). Moreover, in our office we have often made the joke that we are in the tree killing business. Why because it seems that insurance companies feel the need to print reams and reams of paper of stuff that you will likely never read (Gila Insurance Group LLC does not endorse this practice and highly encourages you to read your policy the writer was unwittingly feeling that pragmatism was witty). My favorite is the part of the insurance policy that states this page is left intentionally blank… why?

Insurance companies can rightly be described as technological dinosaurs. I mean for years one company has been extolling the virtues of getting a quote in 15 minutes. On a side note did you know you can get a quote from multiple companies on GilaInsurance.com in just a few minutes as well? Again, dinosaurs. I mean my patience for 30 second in a microwave is almost nil. Don’t even get me started on when the internet decides to have a traffic jam (super highway. It’s supposed to be a super highway, that means no buffering, right?). Moreover, in our office we have often made the joke that we are in the tree killing business. Why because it seems that insurance companies feel the need to print reams and reams of paper of stuff that you will likely never read (Gila Insurance Group LLC does not endorse this practice and highly encourages you to read your policy the writer was unwittingly feeling that pragmatism was witty). My favorite is the part of the insurance policy that states this page is left intentionally blank… why?

That said, increasing insurance companies are getting better at communications. They will text you, email you, mail you, allow you to access their app, and try to get you to sign in to their insurance portal. Basically, all the ways that you are likely to communicate insurance companies will now do. The question is, how do YOU communicate. Because that is the option you need to select.

Insurance companies do tend to send a lot of communication, but once you are a customer you are only likely to receive important documents. Your actual policy, bills, and renewal offers. All things that you should pay attention to. But more importantly, you may be receiving communications where the company may cancel or change the policy. These are thing that you must pay attention to. Why? because Murphey’s law dictates that the day your policy expires is the day you have something happen. State Law dictates how and when insurance companies can cancel a policy, and part of that is that they have to notify you.

While previously it could be said, hey, I was on the road I didn’t get that in the mail. Today there are too many ways that insurance companies communicate with their customer to blame the mail.

Moral of the story is, choose the communication method that works for you and be sure to pay attention to the communications you receive. It might be something annoying, but it might be something important.